This is a difficult question, and here is my opinion.

Many people have asked me this question, and have expressed the thought that our real estate prices are too high. They have claimed this to be caused by the asset bubble for several years now, but so far the bubble still hasn’t busted and housing prices keep increasing.

Let’s first take a look at the stock (along with the mutual fund) market. In 2015, I heard on the radio that some “advisers” were saying that the market had reached the top and would begin to go down. Three years later, the stock market hasn’t gone down yet; even though we know one day it will turn towards the other direction, the problem is when. If we buy now, we may end up buying at top prices and lose money when market goes down, and if we do not buy, we may lose the opportunity of growth. This is why it’s such a tough choice deciding when it will be a good time to invest.

As we have no “crystal ball” to foresee what will happen in the future, most predictions are only “guesses” at best. The economy relies on too many different factors, so it would be best to have a strategy to deal with it.

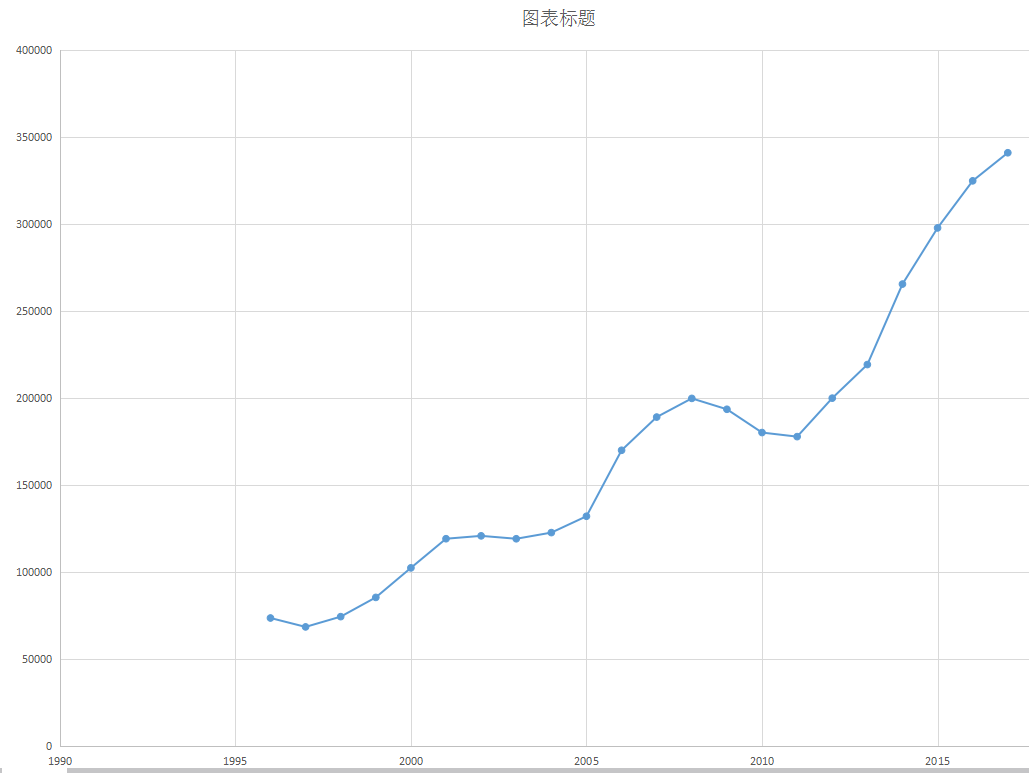

Now, let’s look at what history can tell us. The facts below show the history of average prices for a small area, which is around the first house I bought in the US in 1996.

In 1996, the average price was $73695, and by November 2018, the median price in that area is currently sitting at $342000.

To be fair, I set the radius of house sold in 0.5 miles around the address 4610 Philco Dr, Austin TX 78745, and the house built time must be before 1972 (so the sold houses are similar for comparison purposes). The data is from my own research from Austin board of Realtor MLS system.

Now, knowing this, let’s see the S&P 500 index (data taken from YAHOO finance).

The S&P 500 index includes dividends already, so we can view it as a real reflection of investment return. In the real world, different S&P index funds may have some differences on their returns.

In 1996, the index was 670 and in December 8th. 2018, it has gone up to 2633. That’s 3.9298 times more. That means if you invested $1 in 1996, you would have around $3.93 now.

On the real estate side, if we bought a house (of average condition) in the area in 2006 and decided to sell it now, it should sell for about 4.64 times more.

You might be thinking, “Hey, you forgot about tax, insurance, and maintenance costs.” My response to that will be that the house should not be vacant for most of the time. The rent income should cover all costs such as mortgage, tax, insurance, maintenance, and even bring in positive cash flow.

The above scenario shows that the prices of houses are generally much more stable than those of stocks. When stocks go down, housing prices change much less. Also, do not forget that most people buy houses with loans. Assuming the investor paid 25% down and bought a house then, we can calculate and see how much in returns he can really get.

Assuming the price of the house was $74,000 and closing costs were $3,000, the real out-of-pocket money from the investor was $21,500. He then sold the house last month for $342,000 with a cost of 7%. He needed to pay off the remaining mortgage which was $34,000, and then received $342,000 * 0.93 – 34000 = $284,060 at closing. His investment return is $284,060/21,500 = 13.21 or 1321%.

Of course, the assumption for the above case is that the rent collected will be covering all mortgage, tax, insurance and maintenance costs. However, is this possible in reality? Sure.

In the year 1996, the 30 year fixed rate mortgage rate was about 8.25%, and mortgage payments were $417 per month. Tax was about $166, insurance about $40 (per month), so it came to a total of $623 per month. I then added $50 per month for maintenance cost, which means about $600 per year. By this calculation, the money earned is more than necessary. Total monthly costs were $673 and the rent was about $735 per month back then. Even taking vacancy and management costs into consideration, it should break even or, at worst, leave you with just a little bit of negative cash flow.

Currently the average house rent has increased to $1660 per month, while mortgage payments never increased. Actually mortgage payments have even decreased to some extent, because after 2002, mortgage rates continue to decrease and landlords can opt to refinance to reduce mortgage payments. Even though today’s property tax and insurance payments have increased, with an estimate of tax being $766/month, insurance $120/month, and maintenance costs $100/month, the mortgage payment is reduced to $285 as a result of refinancing and the total monthly payment is $1271. That equals a little more positive cash flow for the landlord than before.

Here we did not consider income tax. As tax brings benefit (depreciation, capital gain tax, 1031 exchange), the real return might be higher.

In real life practice, as recent interest rates are still low (low mortgage payments), the rent to price ratio is lower than before. Houses in this area may be not the best for today’s investment, but would be good if they were purchased in the mid-90s.

My personal view is that we should buy at any time. As we do not know exactly what will happen in future, we can at least assume that in long run, house prices will continue to increase. Of course, a house in Texas will also be much safer than most other investment products.

In 1996, it was a good area to invest in. Is it still good now? I believe so. As there are personal preferences on investments, different people may have different opinions. Above is just my own two cents based on some real life experiences. If you are interested in discussing real estate investments with me, please join me on my social media. or contact me.

Xiaomin James Wu

{kind=link}

{kind=link}

{kind=link}

{kind=link}